January 13, 2021

The National Statistics Institute (INE) released the final figures for inflation in December. We highlight the following:

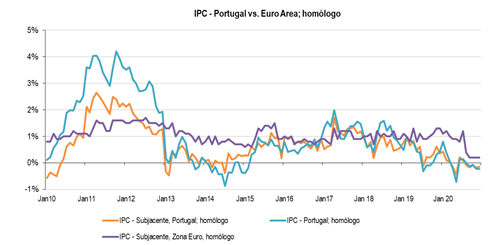

1 - The general price level (CPI) remained in negative territory for the fourth consecutive month, -0.2% homologous, in line with the preliminary values and compared with the average values for the last 12 months (12MMA): - 0.01% and 3MMA: -0.17%;

2 - Underlying inflation (excluding the impact of volatile goods: energy and unprocessed food products): -0.1% homologous, slightly above the preliminary values and the fifth consecutive negative month; compares with 12MMA: -0.04% and 3MMA -0.14%;

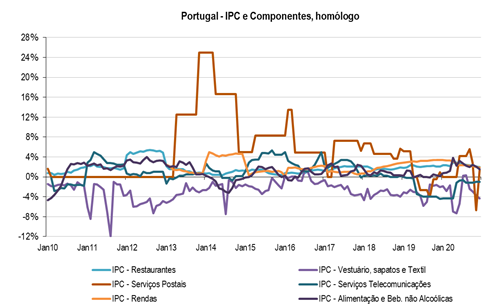

3 - Food and non-alcoholic beverages: + 1.5% homologous vs. 12MMA: + 2.09% and 3MMA: + 2.01% (sequentially: -0.74%);

4 - Restaurants / meals out: + 2.00% homologous vs. 12MMA: + 2.40% and 3MMA: + 2.13% (sequentially: + 0.07%);

5 - Income: + 1.90% homologous vs. 12MMA: + 2.59% and 3MMA: + 2.03% (sequentially: + 0.09%);

6 - Telecommunications: -1.0% homologous vs. 12MMA: -2.12% and 3MMA -1.06% (sequentially: -0.12%);

7 - Clothing and Footwear: -4.40% homologous vs. 12MMA: -3.25% and 3MMA: -3.67%.

The general level of prices in line with the preliminary values, while the underlying inflation, slightly above, although it remains negative, in a consecutive series of 5 months negative and that has not been registered for about 11 years. In general, the price index subcomponents show a modest performance, including the evolution of prices in restaurants and the evolution of rents, two variables, which have registered values above 2%; also show some deceleration, with the last values below the moving averages. In short, we are in a deflationary environment, which, depending on the pace of economic recovery in 2021, may intensify; concretely if the recovery falls short of expectations.

Source: INE, AS Independent Research

António Seladas, CFA

Back