December 16, 2020

Significant changes in terms of short-term policies are not expected, either from a fiscal point of view or by the monetary authorities. The emergence of inflationary pressures in the United States, with a late reaction by the Federal Reserve, could dictate an abrupt fall in the dollar.

In the various texts we have written over the past 12 months, particularly after the pandemic, we have not always been right in the recommendations on the topic of risk. If, at first, once the correction of the markets started as a result of Covid-19, we believed that it would be a good opportunity to buy and reinforce positions in assets with greater associated risk, namely stocks, it is also true that we recommended positions less exposed to equity assets.

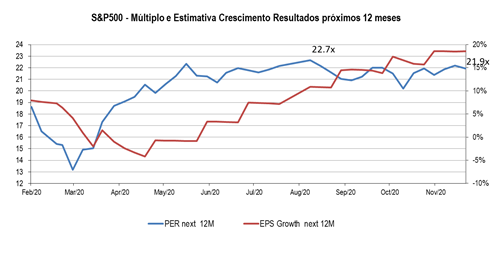

One of the arguments we used in May to justify less exposure to equity risk was the overvaluation of the S&P 500 (one of the main US equity indices), in terms of multiples of the estimated results for the next 12 months, which was above 20x, a high value in absolute and historical terms, this 20x multiple has not been registered since 2002; on the other hand, there was a correlation between the multiple (bottom graph, blue line; left scale) that expanded and the estimated growth in results (bottom graph, red line; right side scale) that contracted. Since then, the multiple has expanded, but at a slower pace, the estimated results for the next 12 months are currently around 22x.

In other words, and in summary, our idea that the pace of expansion of the multiple was running out was correct (blue line), in fact the multiple has barely expanded since then, however, we did not anticipate the excellent performance of the estimated results for the next 12 months (red line); the growth rate of results for the next 12 months has evolved from close to zero in May to around 20% today (red line). There is a mechanical effect over time, but it is undoubtedly the estimates themselves, particularly those for 2020, that are updated upwards. According to Factset (an aggregator of this type of information), the quarterly results for the 2nd Quarter 2020 and 3rd Quarter 2020 surprised, above any record in the past, which is somehow understood, as the pandemic reduced visibility, made the messages cautious and analysts reflected this environment in their estimates, which became excessively pessimistic vs. the final results, which, however, have been released.

Source: Factset, AS Independent Research

Another indicator that we appreciate and which was commented on here in the past is the so-called Implied ERP - Equity Rysk Premium, which works as a kind of cushion, in the sense that investors, when they are afraid of the asset actions, require higher risk premiums and vice versa. This metric, also in May, with the S & P500 close to 2 900 points, recommended a reduction in exposure to equity risk, but in this case to neutral and has since maintained the recommendation. In fact, this indicator takes into account the so-called risk-free interest rates, in the case of the USA, the 10-year State issuance, which is abnormally low (currently close to 0.90%), as a result of strong Federal Reserve interventions. The implicit risk premium rises with the fall of risk-free interest rates, that is, direct interventions by central banks in debt issues through their purchase, increases the market risk premium, everything else constant and, as such, makes stocks more attractive. In fact, central banks with their operations, forcing risk-free interest rates downwards, are encouraging the purchase of shares and the expansion of multiples to historically high levels.

What can we expect for 2021

Inflation levels remain low, despite intense discussion about the possibility of inflation arising as a result of extraordinarily expansionary fiscal and monetary policies and some indicators pointing in that direction, but it remains to be seen whether these types of indicators are rising because there is pressure on prices or if it rises only because the general price level is expected to rise. In this sense, and without the threat of inflation, central banks should maintain their performance, pressing down interest rates, while governments should maintain expansionary fiscal policies, but with smaller deficits and as such in relatively less expansionary terms. In exchange terms, the dollar may have been surprised by its weakness, which was always expected in view of the evolution of its external and public accounts, but was always postponed.

In practice, no significant changes are expected in terms of cyclical policies for 2021, either on the part of the States or on the part of the monetary authorities, with the depreciation of the dollar appears to be an implicit desire of the American authorities, so that, as there are no doubts related to the euro project, the dollar should keep falling.

On the other hand, we are going to enter 2021 with the S&P 500 trading with the estimated 22x results for 2021 and an expected results growth rate for 2021 of about 21%, which gives a PEG (PER ratio, results growth rate multiplied by 100) close to 1x, while the implicit market risk premium stands at 5.70%. Contextualizing, the Multiple is at absolutely high levels, we found this type of values for about 19 years, in the wake of the crisis known as “dot-com bubble”, but the PEG is absolutely in line, eventually, even favorable vs. long-term averages, and ERP, are also at acceptable levels vs. short moving averages and a comfortable area when compared to long moving averages. In other words, the usual metrics to evaluate the stock markets, and in particular the S&P 500, are not conclusive, making it more difficult to predict the performance in 2021. Even so, we note that the share performance of the S & P500 in the last 7 months was closely related to the evolution of results, in fact the S&P 500 rose about 20% while the estimated results for the next 12 months went up by about 17%; the Multiple, meanwhile, expanded a little from 21.3x to 21.9x and the ERP fell about 44bp to 5.70%, but remained in a comfortable zone, while the PEG, as mentioned above, remained , also, in a comfortable zone about 1X.

In summary, the market is apparently not expanding multiples, but rather evolving in line with the variations in expected results; if we are certain in our presumption the performance of the S&P 500 in 2021 will reflect the expected growth of results in 2022. However, if the market did not expand multiples in such a period of strong upward revision of results, as were the last 7 months, if we are facing a moderate period in terms of growth in results, it may require lower multiples (contraction of multiples) and in that sense the performance in 2021 may be modest or negative.

The emergence of inflation, specifically in the USA, could significantly change the dynamics and main scenarios described above. Always depending on the Federal Reserve's reaction, the emergence of inflation with a late reaction by the FED, in the sense that it maintains expansionary monetary policies and causes even more negative real interest rates, the dollar is likely to fall at a high pace and the stock market it will rejoice, and, due to exchange rate appreciation, the rest of the world will suffer. If, on the contrary, the rise in the price level provokes an almost immediate reaction from the Fed, the dollar will tend to appreciate, but the stock market will react negatively. Bearing in mind the recent speeches by the President of the Federal Reserve, Jerome Powell, he should opt for a late reaction, that is, the first scenario.

Article written by:

António Seladas

António Seladas

Back